Mega Funds, Mega Premiums – and the Looming Early-Stage Squeeze in Europe

Mega Funds, Mega Premiums – and the Looming Early-Stage Squeeze in Europe

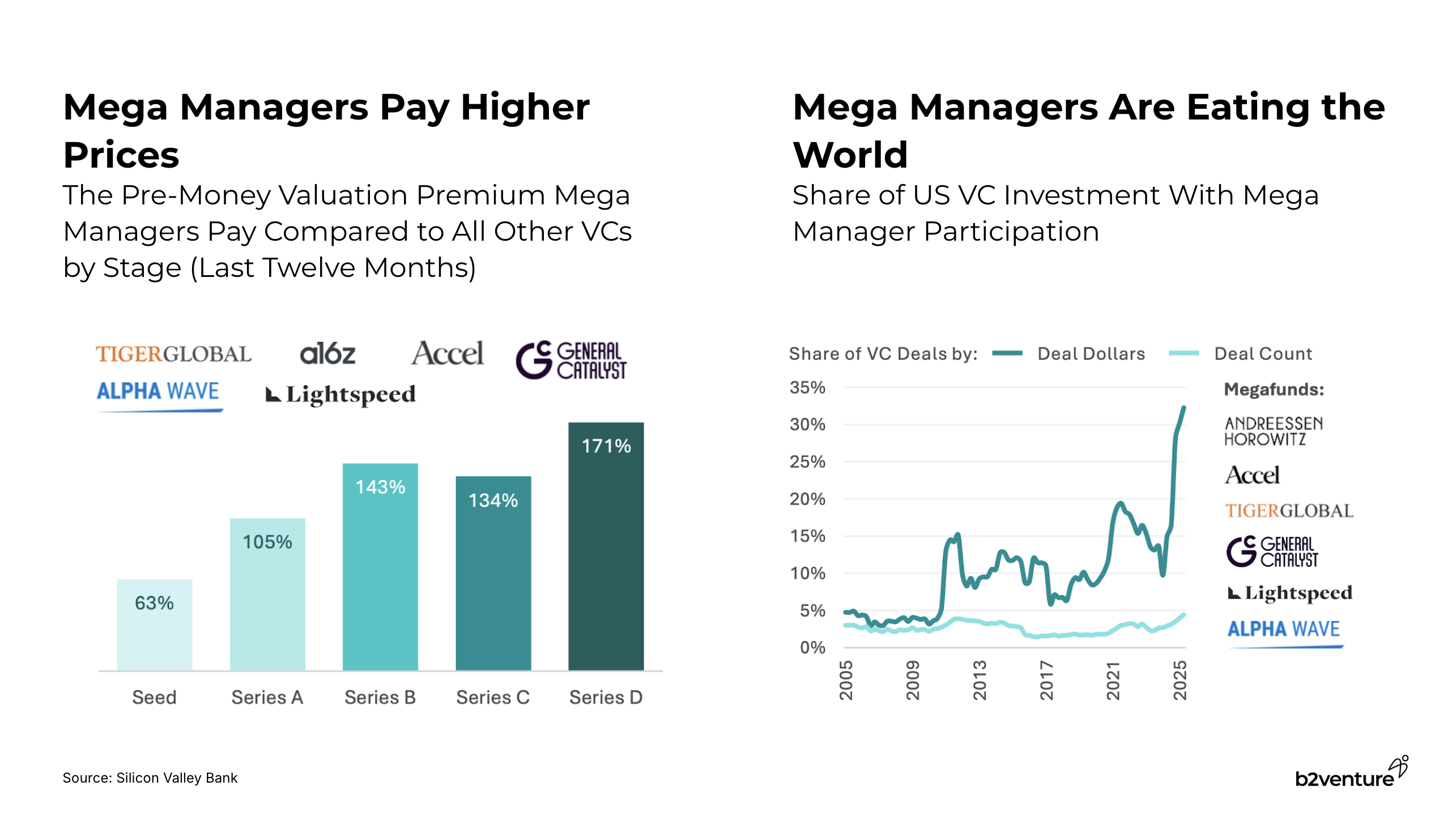

I’ve been thinking a lot lately about a dynamic that's reshaping our industry, and what it means for founders and early-stage investors like ourselves, b2venture. We’re in a strange phase right now—the venture market often feels overheated, particularly in specific verticals like AI, with mega funds pouring record amounts of capital into companies, paying significant valuation premiums compared to everyone else. Or, as Jackie DiMonte recently put it, "mega funds are paying 2–3x higher prices than everyone else," citing the recently published SVB State of the Markets H2 2025 report.

While these numbers are US-centric, my observation is that the same forces are starting to shape Europe’s venture landscape. This is partly because many of these mega funds – including firms like General Catalyst, Lightspeed, and Accel – invest globally and have a strong local presence here in Europe.

The Early-Stage Dilemma

For smaller, early-stage funds, this creates a strategic crossroads. Competing head-on with mega funds on price is often impossible. But rather than a crisis, I see it as a mandate to double down on what truly creates value.

Here are three convictions that guide my thinking in this changing market environment:

1. Experienced Founders Resist the Lure of Overpricing.

In overheated markets, the temptation is to grab the highest number on a term sheet. But seasoned founders know that a bloated valuation can be a poison pill:

- It can lead to unrealistic expectations and future down-round risk.

- It distorts decision-making by pushing for premature scaling.

- It makes the next fundraising story harder to tell.

They understand that the right partner and strategic alignment are far more valuable in the long run than chasing a vanity valuation in the short term. In fact, many experienced founders actively avoid small checks from deep pockets. Christoph Janz, my former boss, colleague, and Founding Partner at Point Nine, has written extensively on the dangers of raising too much too early from stage-agnostic investors - it’s an evergreen topic in the VC community (his classic blog post here).

2. Valuation- & Terms-Discipline Pays Off.

Paying up to “stay in the game” might feel necessary, but for early-stage funds, discipline matters – both for fund math and LP trust. In the short term, walking away from an overheated deal can be painful. But, speaking from my own experience, over the long run, sticking to your strategy and price discipline is what keeps a fund’s performance intact. After all, our primary duty is to our LPs and to the companies we back. They, too, deserve a long-term sustainable strategy.

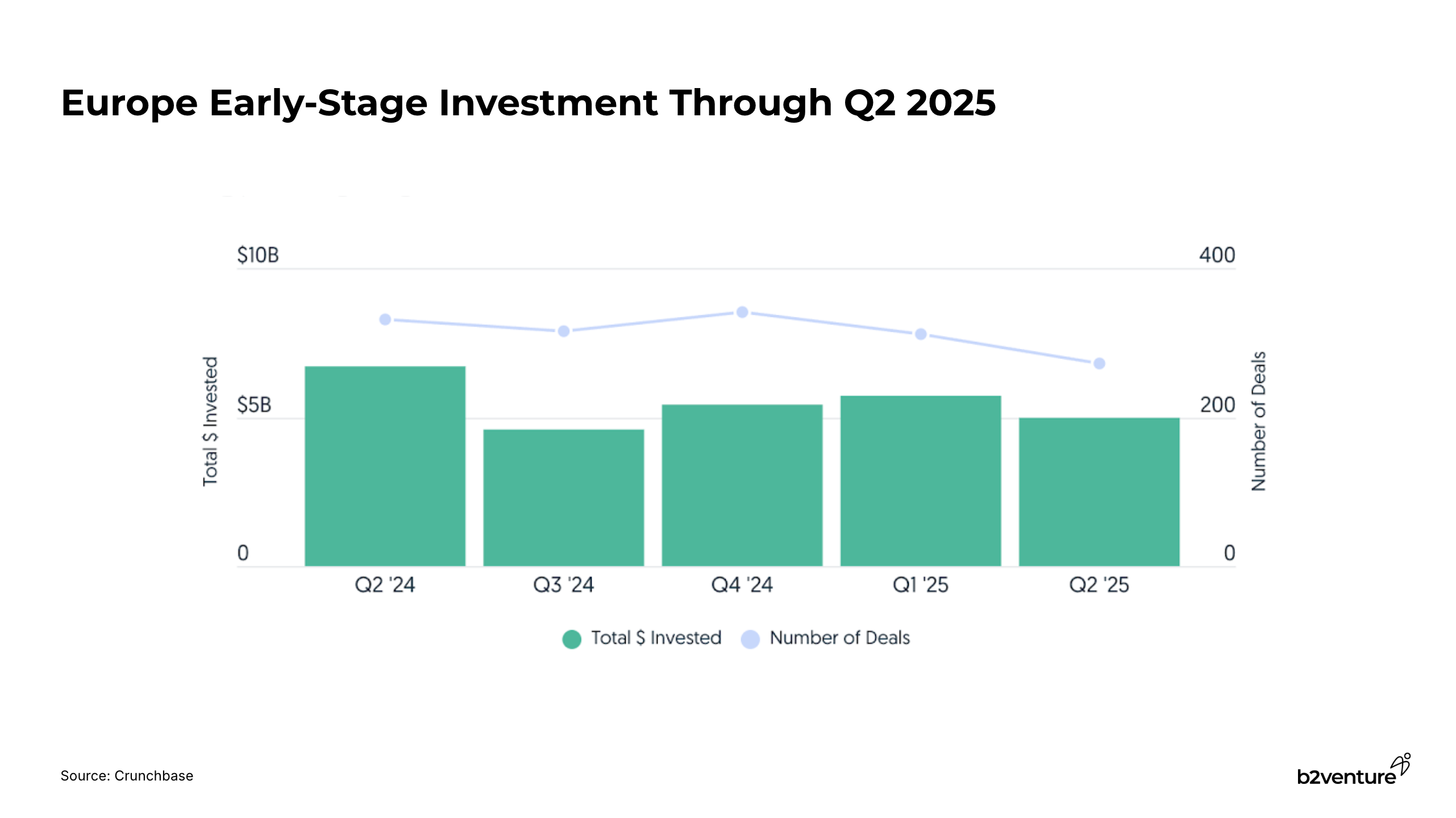

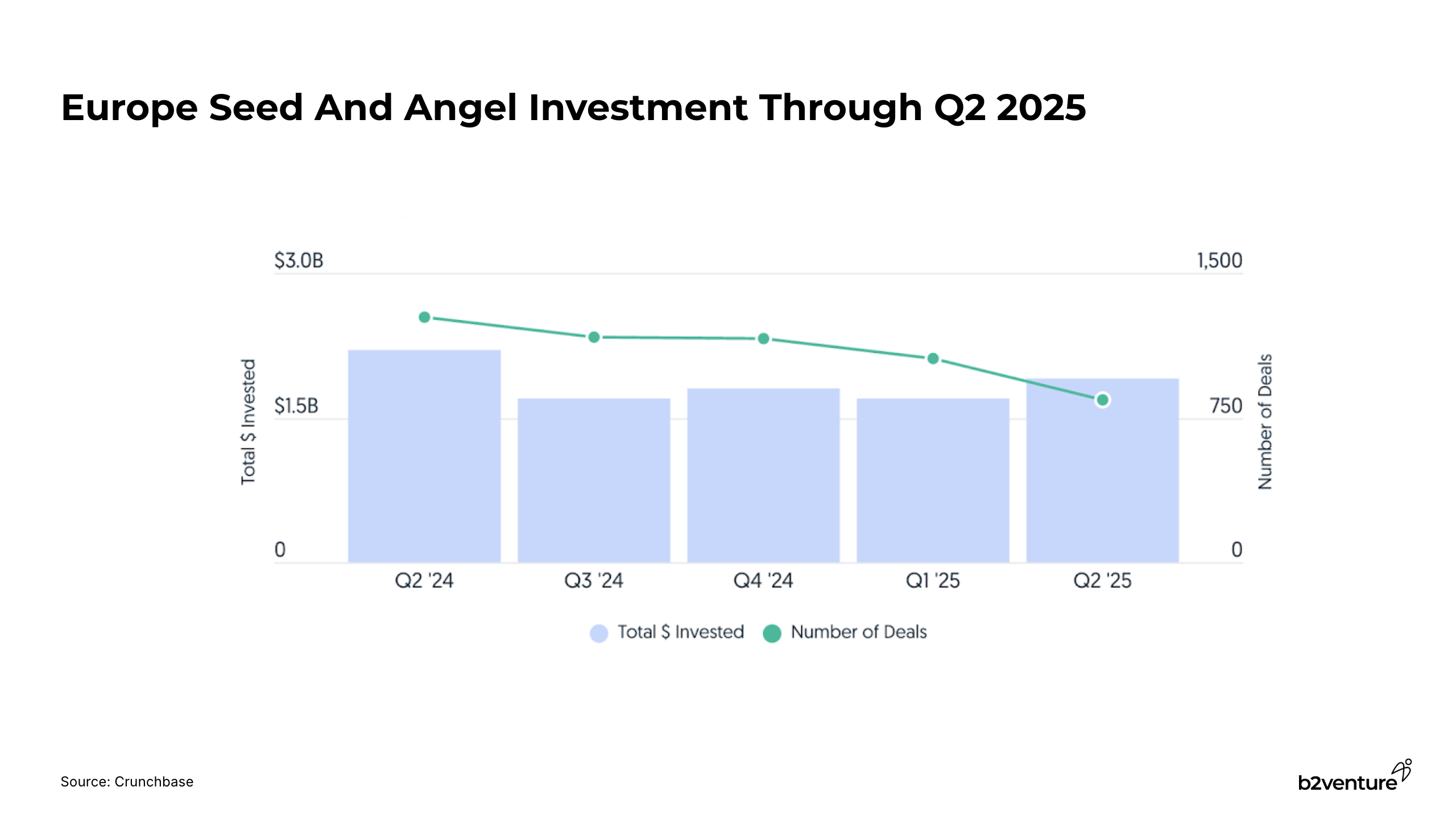

As the Crunchbase H1 2025 European VC funding report shows, while European Angel and Seed funding volumes in the first half of the year remained stable compared to the second half of last year (approx. +2.9%), the number of deals dropped by over 18%. This means, in Europe too, more capital is being concentrated in fewer companies, which likely pushes valuations higher for those who do get funded. This, in turn, makes valuation discipline harder – and more important than ever.

3. Keep Investing – More Than Just Capital.

A market frenzy or a new competitive dynamic is not a reason to stop investing. Venture is a long term game, and portfolio diversification also happens over time. But investing on your terms not only means staying disciplined on terms, but also finding and owning your niche and your own approach. This is where smaller, specialized funds shine. For mega funds, their primary competitive edge at the early stage is often a single dimension: capital. They compete by being less price-sensitive and offering substantial valuation premiums. Smaller funds simply can’t – and shouldn’t – compete on that basis. Their competitive edge has to be built on something else, something that money cant buy. If you can’t (or won’t) win on price, win on value:

- Beyond Capital: It’s about more than just money. It’s about offering deep sector focus, specific domain expertise, and access to unique networks. At b2venture, for example, our angel network provides founders with unparalleled access to industry leaders and domain specialists who can offer help beyond what capital alone can buy.

- Vertical specialization: Point Nine Capital, NFX, Zeroprime Ventures, Backtrace.

- Broad early-stage network: Seedcamp.

- Community-driven local ecosystem building: LocalGlobe.

- Fast, high-volume Angel-style investing: Angel Invest, Kima Ventures.

VC Is a People Business: You’re not just raising from “a fund” – you’re partnering with specific individuals who may stay with you longer than most marriages last (that end in a divorce). Early-stage relationships are more personal: smaller teams, more stability, and deeper founder–investor alignment not just personally but also financially (more on that below). In smaller funds, teams are usually more stable and personal. With mega funds, team turnover is higher and relationships can get diluted, in particular if that comparatively small check in your tiny early-stage company has to compete for attention with other, much larger investments of the same fund and investor. No founder wants to end up as an “orphaned startup” without an engaged sponsor. This human element is a competitive advantage for smaller players.

Strong Financial Alignment: Beyond the “human” element, there is another argument in favor of smaller early-stage funds from a founders point of view: As valuation and follow-on funding increase over time, early-stage investors’ entry points tend to converge with founders’ economics, creating stronger long-term alignment compared to later stage investors. That can matter significantly when it comes to a potential liquidity event in particular regarding liquidation preferences and voting rights. Tying this back to my previous point, this inherent dynamic further underlines the importance of choosing the right people to work with – those that support your cause as a founder and can help make the right calls when and if needed.

Why Europe is Different

Proponents of the mega fund model argue that these premiums are justified by a focus on quality and the winner-take-most dynamics of network effects-driven businesses.

The logic behind the quality argument is that the largest outliers generate such outsized returns that paying a premium is still worth the chance to participate in these highest-quality companies. Indeed, in the US, the frequency of billion-dollar-plus exits is at a record high. However, Europe’s reality is different. Mega outcomes are much rarer and smaller compared to the US. Applying the US playbook of paying top dollar for potential outliers might not work the same way here.

Similarly, the network effects argument is often overblown. Many businesses that claim to benefit from future network effects never develop any, as they didn’t have these dynamics to begin with. Everyone wants to become a “platform” - even in the AI age - but very few actually can and even fewer do.

In any case, the SVB report notes that for all AI companies - a major focus for these mega funds - it will take several years to see if the eye-popping valuations translate into real returns. The jury is still out.

The real risk is to the ecosystem itself. If too much capital concentrates in a handful of multi-stage funds, we risk crowding out an entire generation of early-stage investors. This would not only reduce the diversity of capital, but also hurt the very deal flow that mega funds rely on, essentially “killing the hand that feeds them”.

Closing thought

The big question remains: Is the current valuation premium paid by mega funds a new, sustainable reality, a passing phase that will correct itself, or a symptom of an overheated market? The next few years will tell. As Sam Altman put it in a recent TheVerge interview, we may well be in the midst of an AI bubble or heading towards one. This may be a risk all investors are taking, but a correction would validate the discipline and differentiated approach as described above.

Ultimately, the overall VC and tech startup market is large and dynamic enough to support different approaches without these players getting in each others way. The ecosystem is not a zero-sum game, and the various players –from niche micro-funds to global mega-managers –can coexist and thrive by focusing on their unique value propositions.

Join Our Team

If you believe, as we do, that building a winning fund is about more than just capital, we want to hear from you. We are looking for an Analyst or Associate to join our investment team and help us build the future of European venture.

Learn more and apply here.

Sources & Further Reading:

- Jackie's post

- SVB State of the Markets H2 2025 report

- Should you take small checks from deep pockets?

- Crunchbase H1 2025 European VC funding report

- TheVerge "Sam Altman says ‘yes,’ AI is in a bubble"

- Leslie Feinzaig & Carta's Peter Walker on the current state of the market

I’ve been thinking a lot lately about a dynamic that's reshaping our industry, and what it means for founders and early-stage investors like ourselves, b2venture. We’re in a strange phase right now—the venture market often feels overheated, particularly in specific verticals like AI, with mega funds pouring record amounts of capital into companies, paying significant valuation premiums compared to everyone else. Or, as Jackie DiMonte recently put it, "mega funds are paying 2–3x higher prices than everyone else," citing the recently published SVB State of the Markets H2 2025 report.

While these numbers are US-centric, my observation is that the same forces are starting to shape Europe’s venture landscape. This is partly because many of these mega funds – including firms like General Catalyst, Lightspeed, and Accel – invest globally and have a strong local presence here in Europe.

The Early-Stage Dilemma

For smaller, early-stage funds, this creates a strategic crossroads. Competing head-on with mega funds on price is often impossible. But rather than a crisis, I see it as a mandate to double down on what truly creates value.

Here are three convictions that guide my thinking in this changing market environment:

1. Experienced Founders Resist the Lure of Overpricing.

In overheated markets, the temptation is to grab the highest number on a term sheet. But seasoned founders know that a bloated valuation can be a poison pill:

- It can lead to unrealistic expectations and future down-round risk.

- It distorts decision-making by pushing for premature scaling.

- It makes the next fundraising story harder to tell.

They understand that the right partner and strategic alignment are far more valuable in the long run than chasing a vanity valuation in the short term. In fact, many experienced founders actively avoid small checks from deep pockets. Christoph Janz, my former boss, colleague, and Founding Partner at Point Nine, has written extensively on the dangers of raising too much too early from stage-agnostic investors - it’s an evergreen topic in the VC community (his classic blog post here).

2. Valuation- & Terms-Discipline Pays Off.

Paying up to “stay in the game” might feel necessary, but for early-stage funds, discipline matters – both for fund math and LP trust. In the short term, walking away from an overheated deal can be painful. But, speaking from my own experience, over the long run, sticking to your strategy and price discipline is what keeps a fund’s performance intact. After all, our primary duty is to our LPs and to the companies we back. They, too, deserve a long-term sustainable strategy.

As the Crunchbase H1 2025 European VC funding report shows, while European Angel and Seed funding volumes in the first half of the year remained stable compared to the second half of last year (approx. +2.9%), the number of deals dropped by over 18%. This means, in Europe too, more capital is being concentrated in fewer companies, which likely pushes valuations higher for those who do get funded. This, in turn, makes valuation discipline harder – and more important than ever.

3. Keep Investing – More Than Just Capital.

A market frenzy or a new competitive dynamic is not a reason to stop investing. Venture is a long term game, and portfolio diversification also happens over time. But investing on your terms not only means staying disciplined on terms, but also finding and owning your niche and your own approach. This is where smaller, specialized funds shine. For mega funds, their primary competitive edge at the early stage is often a single dimension: capital. They compete by being less price-sensitive and offering substantial valuation premiums. Smaller funds simply can’t – and shouldn’t – compete on that basis. Their competitive edge has to be built on something else, something that money cant buy. If you can’t (or won’t) win on price, win on value:

- Beyond Capital: It’s about more than just money. It’s about offering deep sector focus, specific domain expertise, and access to unique networks. At b2venture, for example, our angel network provides founders with unparalleled access to industry leaders and domain specialists who can offer help beyond what capital alone can buy.

- Vertical specialization: Point Nine Capital, NFX, Zeroprime Ventures, Backtrace.

- Broad early-stage network: Seedcamp.

- Community-driven local ecosystem building: LocalGlobe.

- Fast, high-volume Angel-style investing: Angel Invest, Kima Ventures.

VC Is a People Business: You’re not just raising from “a fund” – you’re partnering with specific individuals who may stay with you longer than most marriages last (that end in a divorce). Early-stage relationships are more personal: smaller teams, more stability, and deeper founder–investor alignment not just personally but also financially (more on that below). In smaller funds, teams are usually more stable and personal. With mega funds, team turnover is higher and relationships can get diluted, in particular if that comparatively small check in your tiny early-stage company has to compete for attention with other, much larger investments of the same fund and investor. No founder wants to end up as an “orphaned startup” without an engaged sponsor. This human element is a competitive advantage for smaller players.

Strong Financial Alignment: Beyond the “human” element, there is another argument in favor of smaller early-stage funds from a founders point of view: As valuation and follow-on funding increase over time, early-stage investors’ entry points tend to converge with founders’ economics, creating stronger long-term alignment compared to later stage investors. That can matter significantly when it comes to a potential liquidity event in particular regarding liquidation preferences and voting rights. Tying this back to my previous point, this inherent dynamic further underlines the importance of choosing the right people to work with – those that support your cause as a founder and can help make the right calls when and if needed.

Why Europe is Different

Proponents of the mega fund model argue that these premiums are justified by a focus on quality and the winner-take-most dynamics of network effects-driven businesses.

The logic behind the quality argument is that the largest outliers generate such outsized returns that paying a premium is still worth the chance to participate in these highest-quality companies. Indeed, in the US, the frequency of billion-dollar-plus exits is at a record high. However, Europe’s reality is different. Mega outcomes are much rarer and smaller compared to the US. Applying the US playbook of paying top dollar for potential outliers might not work the same way here.

Similarly, the network effects argument is often overblown. Many businesses that claim to benefit from future network effects never develop any, as they didn’t have these dynamics to begin with. Everyone wants to become a “platform” - even in the AI age - but very few actually can and even fewer do.

In any case, the SVB report notes that for all AI companies - a major focus for these mega funds - it will take several years to see if the eye-popping valuations translate into real returns. The jury is still out.

The real risk is to the ecosystem itself. If too much capital concentrates in a handful of multi-stage funds, we risk crowding out an entire generation of early-stage investors. This would not only reduce the diversity of capital, but also hurt the very deal flow that mega funds rely on, essentially “killing the hand that feeds them”.

Closing thought

The big question remains: Is the current valuation premium paid by mega funds a new, sustainable reality, a passing phase that will correct itself, or a symptom of an overheated market? The next few years will tell. As Sam Altman put it in a recent TheVerge interview, we may well be in the midst of an AI bubble or heading towards one. This may be a risk all investors are taking, but a correction would validate the discipline and differentiated approach as described above.

Ultimately, the overall VC and tech startup market is large and dynamic enough to support different approaches without these players getting in each others way. The ecosystem is not a zero-sum game, and the various players –from niche micro-funds to global mega-managers –can coexist and thrive by focusing on their unique value propositions.

Join Our Team

If you believe, as we do, that building a winning fund is about more than just capital, we want to hear from you. We are looking for an Analyst or Associate to join our investment team and help us build the future of European venture.

Learn more and apply here.

Sources & Further Reading:

- Jackie's post

- SVB State of the Markets H2 2025 report

- Should you take small checks from deep pockets?

- Crunchbase H1 2025 European VC funding report

- TheVerge "Sam Altman says ‘yes,’ AI is in a bubble"

- Leslie Feinzaig & Carta's Peter Walker on the current state of the market

The Author

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

-min.png)

.jpg)

.jpg)